2017 Tax Reform Proposal: Too Simple?

Einstein is often quoted (maybe incorrectly) as saying "Everything should be made as simple as possible, but not simpler." I couldn't agree more with this expression and am always trying to simplify complex topics for clients. Whether that means translating the abstract language often found in our tax code or deciphering pages of disclosures in complicated investment vehicles; simple is usually better. Two of my favorite finance books are "Simple Money" by Tim Maurer and "The One Page Financial Plan" by Carl Richards. So you might expect me to be pleased with the tax reform plan presented by the White House on Wednesday, April 26, 2017:

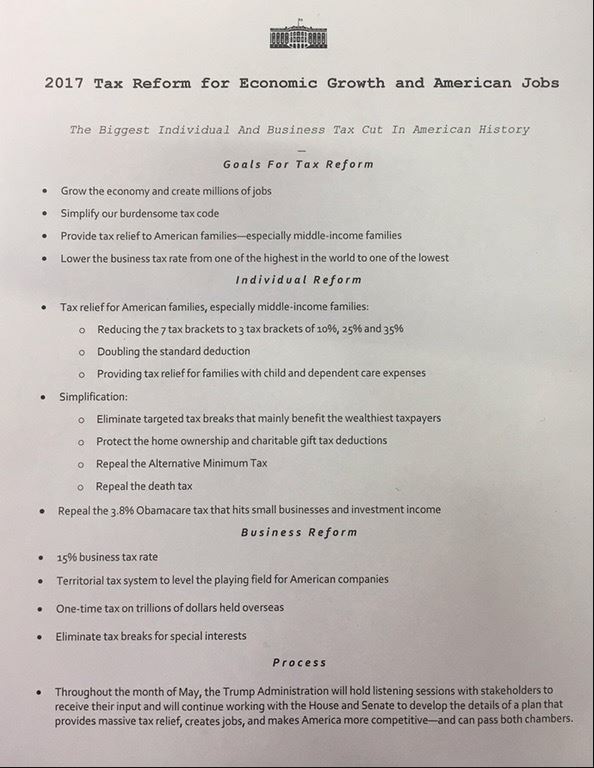

If there's one word to describe the plan, simple might be it. One page and less than 125 words. Heck, one of the sections is even titled "Simplification"!

Unfortunately in this case I think the plan might be a little too simple. The tax code is incredibly complex so any plan to simplify it will need to be much more detailed. Given this lack of details it's hard to truly evaluate the impact or make any judgement over the potential for the plan to be enacted. The Trump administration made it clear the details will be worked out over the coming months through discussions and negotiations with the House and Senate so we will continue to stand by and monitor those discussions.

In the meantime, there are some important items to note in this plan that might give us some insight into any legislation that could eventually be passed:

- Business Tax Rate - The proposed business tax rate of 15% is a major reduction from the current 35% and would move the U.S. from being one of the highest taxed countries in the developed world to one of the lowest.

- Pass Through Entities - The plan doesn't specifically mention pass through entities, but as a candidate President Trump included a provision in his plan that would allow owners of pass through entities to be taxed at the proposed business tax rate. While Treasury Secretary Steve Mnuchin did say they would close any loopholes this might create, it will be interesting to see how they move forward on this key issue that will impact many of our clients.

- Individual Tax Brackets - As expected, the plan outlines a consolidation from the current 7 bracket tax structure to just 3 brackets: 10%, 25% and 35%. No details were given on where the income levels would fall for the brackets.

- Alternative Minimum Tax - The plan proposes repealing the AMT completely.

- Net Investment Income Tax - The plan also proposes repealing the 3.8% surtax on net investment income that has been in place since the Affordable Care Act was passed.

- Estate Tax - A full repeal of the estate tax is also proposed, though no details are given as to the continued step up in basis at death or a potential capital gains tax at death as had been mentioned previously.

- Itemized Deductions - The standard deduction would double under the proposal and mortgage interest and charitable contribution deductions would remain in tact, but could be limited. It does appear other deductions, like the state income tax deduction, could be eliminated. This could have a huge impact for many, especially residents of high-tax states like California and New York.

It would appear the administration has a long way to go before they can accomplish any meaningful tax reform. As it is currently constructed, this proposal would result in a massive increase in the federal deficit and that will make it difficult to garner enough support to be passed into law. Most policy experts are skeptical the administration will be able to put together a plan that can be passed this year but that remains to be seen. Any tax reform close to what was outlined in this plan would result in major changes to the tax and financial planning we do for our clients. We will continue to closely monitor these discussions and keep you up to date on any progress.

For more reading on the tax reform plan, here are some additional resources:

http://www.journalofaccountancy.com/news/2017/apr/trump-tax-priorities-tax-reform-201716547.html

https://www.accountingtoday.com/news/trump-tax-proposal-draws-mixed-reactions-from-experts

https://www.wsj.com/articles/how-donald-trumps-tax-plan-affects-households-1493236758

The views expressed represent the opinions of L.K. Benson & Company and are subject to change. These views are not intended as a forecast, a guarantee of future results, investment recommendation, or an offer to buy or sell any securities. The information provided is of a general nature and should not be construed as investment advice or to provide any investment, tax, financial or legal advice or service to any person.

Please see Additional Disclosures more information.