Beerflation

I recently had the pleasure of presenting a virtual webinar for my fellow alumni from Bucknell University. I was asked to present on 10 personal finance tips for new graduates. As I started to put together my notes for the presentation I quickly realized I had way more tips than I could fit in a 30 minute presentation. So I did what any good presenter would do - cut my list down to 10, then added a slide with my "bonus tips" so I wouldn't have to leave too much out!

I'll give you my full list in another blog post, but today I wanted to touch on one of my favorite tips from the presentation. The tip was to "minimize your lifestyle inflation". It's something I believe is crucial to your financial success, and something that needs to be understood at a young age. So what is "lifestyle inflation"? Let's start with the term "inflation".

"Back in my day a soda only cost a nickel!" You've probably heard someone say it. Heck, you might have even been the one who said it! This statement represents an easy way to understand inflation. Inflation is simply the increase in prices over time. The government has a number of ways to measure this, but the most common is the Consumer Price Index, or CPI for short. This index tracks the price of numerous consumer goods over time.

Many people argue about how effective CPI is at really measuring the rise of prices over time, but everyone agrees that over time, prices of most consumer goods do generally go up. Some prices go up faster than others - like college tuition. Some might go up slower, or at times even trend downward - like electronics. But we know that inflation is real and it's something that we need to contend with when planning out our future finances. It's the reason we can't be content just parking our savings in cash. If prices rise, the value of that cash actually decreases every year.

But my tip to recent graduates was not to worry about inflation - a factor which is largely out of their control. Instead it was to worry about their own personal "lifestyle inflation". This refers to the increase in what you spend as your income rises. Naturally when we were younger we didn't go out to lavish dinners or go on expensive trips too frequently. But as your income rises your propensity to spend on these things also rises

In my attempt to better illustrate lifestyle inflation, I starting trying to think of examples. Maybe I had a beer in my hand that day, or maybe when I reminisce about college, the first thing that comes to mind is beer (sorry mom and dad!). For whatever reason, I started thinking about how much more I typically spend on a beer these days than I did back then, so I thought I'd put it in chart form:

Now granted, I might have been drinking a little more "in bulk" back in those days, so even though my beer is much more expensive now I'm also not drinking nearly as much of it (having kids will do that to you!). But this still helps to illustrate my point. A case of natural light might be slightly more expensive today than it was 12(!) years ago when I left college, and that would be an example of inflation. But as I've grown in my career and my income has risen, I've become what my wife politely calls a "beer snob" and now buy much more expensive beers than I used to. THAT is lifestyle inflation!

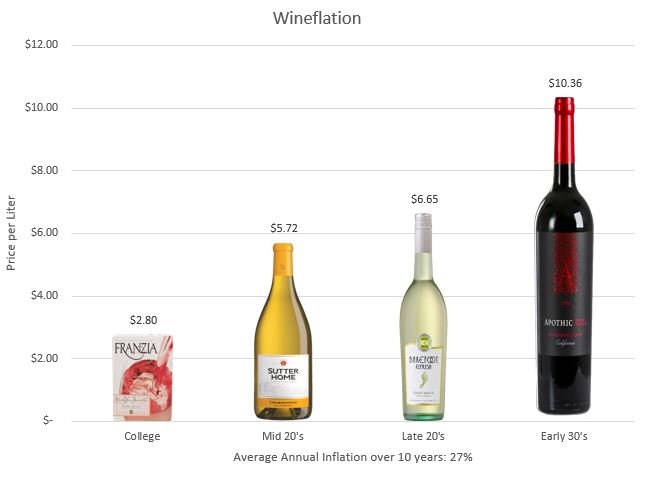

Maybe you aren't a beer drinker and prefer wine. Don't worry I didn't leave you out:

These charts aren't exact representations. They might overestimate or maybe even underestimate what your own personal inflation rate has been. Maybe you didn't start with Franzia or Natural Light, or maybe you are still drinking Yuengling or Barefoot wine. Or maybe you've gone beyond the chart. I know I didn't stop with Dogfish Head 60 minute. I typically go for their Burton Baton or Palo Santo Marron, which are both much more expensive, but I digress.

So we know that lifestyle inflation will happen and I'm not saying you need to stop it completely. Trust me, I'm not going back to sipping on a Natural Light if I need a cold one on the weekend. If we can't stop it, the question becomes how do we control it? Here are a few tips:

- Automate your future savings. As I wrote a couple years ago, one of the easiest ways to keep yourself from increasing your spending too much is to commit to saving more when you get raises. This is easy to do if you have a 401(k) plan - many now offer the option of automatically increasing your savings rate each year. If you don't have that option, just remember to go in to do it yourself.

- Identify what's important to you. As Carl Richards says, your budget should align with your values. It's ok to splurge on some things, but make sure they are important to you. Beer might not be the best example here, but let's look at another area my family has increased their spending - travel. We take several trips a year and believe the experiences we have travelling are way more important than some of the other frivolous things we could be buying with our money.

- Identify spending areas that you can keep in check. I really enjoy a good beer, and for that reason I don't mind spending a little more on that portion of my budget. I don't really get any extra satisfaction out of going out to dinner at a fancy restaurant. So we rarely splurge on a fancy meal out and when we do go out my meals usually come off the "sandwiches" or "salads" section of the menu, instead of the "entrees" section.

- Take time to think about big ticket items. A new house or a new car that will lead to a substantial increase in your monthly expenses is infinitely more important than worrying about the increase in what you spend on beer or wine. Make sure you plan for these types of purchases and make sure it fits in your budget.

- Save 50% of every bonus. If you don't consider your bonus money as part of your regular income, it becomes much easier to just put away a portion of it every year. This helps in two ways. One, it increases your savings. Two, it decreases your lifestyle inflation. It's a win win!

Lifestyle inflation is going to happen regardless of the precautions you take. It's natural and you shouldn't feel guilty of it. But there are things you can do to minimize the impact that will help you out in the long run. Just being aware of it's presence might even be enough to help.

-Chris Benson, CPA, PFS

The views expressed represent the opinions of L.K. Benson & Company and are subject to change. These views are not intended as a forecast, a guarantee of future results, investment recommendation, or an offer to buy or sell any securities. The information provided is of a general nature and should not be construed as investment advice or to provide any investment, tax, financial or legal advice or service to any person.Please see Additional Disclosures more information.